⬤ CPA-Led Entity Guidance

What Is an LLC? Types, Taxes, Equity, and How a Limited Liability Company Really Works

The limited liability company is the most popular business structure in the United States for a simple reason: it wraps the liability shield of a corporation around the tax flexibility of a partnership. But that flexibility cuts both ways.

On this page

This guide explains the LLC from the ground up: what it is, the types you can form, how the taxes actually flow, how owners and employees can hold equity, and how an LLC stacks up against a corporation. We have written it the way we would explain it across a desk – plainly first, then with the detail your CPA or counsel will want.

What an LLC actually is

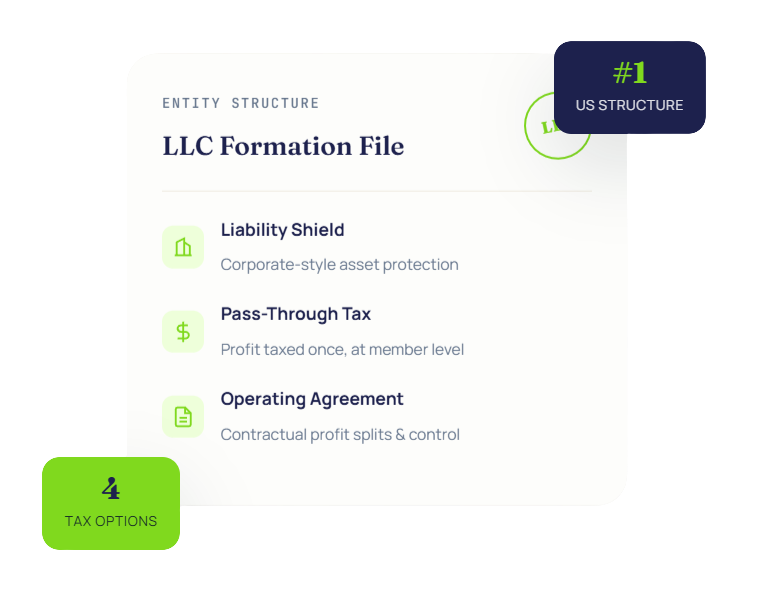

A limited liability company (LLC) is a legal entity formed under state law that separates the business’s assets and obligations from the personal assets of its owners. The owners of an LLC are called members, and their stakes are called membership interests or units rather than shares of stock.

The easiest way to understand an LLC is as a hybrid. From the corporation, it borrows the liability shield: if the business is sued or cannot pay its debts, creditors generally pursue the company’s assets, not the members’ homes or savings. From the partnership, it borrows pass-through taxation: by default, the LLC itself pays no federal income tax. Profit and loss flow through to the members, who report their shares on their own returns.

One more feature sets the LLC apart from both of its parents: almost everything about how it operates is contractual. The operating agreement – the internal document the members sign – decides who manages the company, how profits are split, what happens when a member leaves, and how new members are admitted. Two LLCs with identical state filings can work in completely different ways because their operating agreements say different things.

A worked example

Three friends start a design studio as an LLC and agree in the operating agreement to split profits 50/30/20 – even though each contributed the same amount of cash – because one of them works full-time and the others part-time. A corporation would struggle to do this without creating separate share classes; an LLC does it with a paragraph in the agreement. That contractual freedom is the structure’s defining trait.

How the liability shield works - and how it breaks

Limited liability means a member’s financial exposure is generally capped at what they have invested in the company. If the LLC borrows money it cannot repay, or loses a lawsuit it cannot cover, the members’ personal assets stay out of reach.

The shield is real, but it is not unconditional. Courts can set it aside – a doctrine known as piercing the veil – when the members treat the company as an extension of themselves. The most common ways owners lose the protection:

Commingling funds. Paying personal expenses from the business account, or vice versa, is the classic mistake. Keep separate bank accounts and clean books from day one.

Personal guarantees. Lenders and landlords often require members to personally guarantee loans or leases. A guarantee is a voluntary waiver of the shield for that obligation.

Personal wrongdoing. The LLC does not protect a member from liability for their own negligence or fraud. It protects you from the business's obligations, not from your own conduct.

Undercapitalization and missed formalities. Running the company with no realistic capital, or ignoring required state filings, gives a court reasons to look through the entity.

The main types of LLCs

All LLCs share the same DNA, but they come in several configurations. The right one depends on how many owners there are, what the business does, and who runs it day to day.

Single-member LLC

An LLC with one owner. For federal tax purposes it is a disregarded entity by default — the IRS ignores it, and the owner reports the business on their personal return as if it were a sole proprietorship. The liability shield, however, is fully intact under state law. This is the most common starting point for freelancers, consultants, and solo founders who want protection without complexity.

Multi-member LLC

An LLC with two or more members. By default it is taxed as a partnership: the company files an information return, and each member receives a Schedule K-1 showing their share of profit or loss to report personally. The operating agreement carries the most weight here, because it governs how those shares are calculated and what each member can and cannot do.

Member-managed vs. manager-managed

This is a management split rather than a separate entity type, but it matters. In a member-managed LLC, every owner has authority to act for the company — fine for a two-person shop, risky for a company with passive investors. In a manager-managed LLC, the members appoint one or more managers (who may or may not be members) to run operations, and the other members step back into an investor role.

Professional LLC (PLLC)

Many states require licensed professionals – physicians, attorneys, accountants, architects – to use a professional LLC instead of a standard one. A PLLC shields members from the business’s general obligations, but no structure shields a professional from liability for their own malpractice.

Series LLC

Available in a minority of states, a series LLC is a single parent entity that can create internal cells – series – each with its own assets, members, and liabilities, walled off from the others. Real estate investors use them to hold each property in its own series without forming a separate LLC for each. The structure is powerful but unevenly recognized across state lines, so it needs careful legal advice before you rely on the internal walls.

Domestic vs. foreign LLC

These labels confuse people: foreign here means out-of-state, not out-of-country. An LLC is domestic in the state where it was formed and foreign everywhere else it registers to do business. If you form in one state and operate in another, expect to register as a foreign LLC there and pay that state’s fees too.

How LLCs are taxed: the default and the elections

Here is the single most misunderstood fact about LLCs: the IRS has no LLC tax category. An LLC is a creature of state law, and federal tax law simply asks which existing category it should be slotted into. That gives an LLC something no corporation has – a menu.

|

Tax treatment

|

Who it applies to

|

How profit is taxed

|

|---|---|---|

|

Disregarded entity (default)

|

Reported directly on the owner's personal return, like a sole proprietorship; profit is generally subject to self-employment tax

|

|

|

Partnership (default)

|

Entity files an information return; each member reports their share via Schedule K-1 on their own return

|

|

|

S corporation (by election)

|

Eligible LLCs that file the election

|

Pass-through, but owner-employees take a reasonable salary through payroll; remaining profit distributes without self-employment tax

|

|

C corporation (by election)

|

Any LLC that files the election

|

The entity pays corporate income tax itself; owners pay tax again on dividends they receive

|

The default: pass-through

Under the default rules, the LLC’s profit lands on the members’ personal returns whether or not any cash was distributed. This surprises new owners every year: if the company earns a profit and reinvests every dollar, the members still owe tax on their shares. Well-run LLCs plan tax distributions – cash paid out specifically so members can cover the tax on profit they were allocated.

A worked example

Two members own an LLC 60/40. The company earns $100,000 of profit this year and keeps all of it in the business to fund growth. At tax time, the 60% member reports $60,000 of income and the 40% member reports $40,000 – even though neither received a distribution. These are illustrative figures only; the principle, not the numbers, is the point.

The self-employment tax wrinkle

For a default-taxed LLC, an active member’s share of profit is generally subject to self-employment tax – the equivalent of both halves of Social Security and Medicare – on top of income tax. This is the cost of pass-through simplicity, and it is the main reason profitable LLCs consider the next option.

The S corporation election

An eligible LLC can elect to be taxed as an S corporation while remaining an LLC under state law. The owner then becomes an employee of their own company, takes a reasonable salary through payroll (which bears employment taxes), and receives the remaining profit as distributions that do not. The IRS polices the word reasonable: setting an artificially low salary to push more profit into distributions is one of the most commonly audited small-business positions. The election also brings payroll administration and stricter ownership rules, so it earns its keep only once profits are meaningfully above what a fair salary for the work would be.

The C corporation election

An LLC can also elect to be taxed as a C corporation, paying tax at the entity level. Few small LLCs choose this voluntarily – it introduces the double taxation pass-throughs exist to avoid – but it appears in two situations: companies reinvesting all profit at the entity level, and LLCs preparing to take institutional venture capital, which generally requires C corporation treatment or a full statutory conversion.

Don't forget the state layer

Federal pass-through does not mean tax-free at the state level. Several states impose annual franchise taxes, gross-receipts taxes, or flat LLC fees regardless of profit, and a few do not follow the federal S election at all. The state where you form and the states where you operate both matter.

Equity in an LLC: how owners and employees hold a stake

Corporations issue stock; LLCs issue whatever the operating agreement says. That freedom produces several distinct instruments, and the differences between them are mostly tax differences.

Membership units (capital interests)

The basic ownership unit of an LLC, analogous to common shares of a corporation. A capital interest entitles the holder to a slice of everything the company is worth today plus future growth. Granting a capital interest to someone in exchange for services is generally a taxable event for the recipient – they have received something of present value – which is exactly why the next instrument exists.

Profits interests

The profits interest is the LLC world’s answer to the stock option, and it is arguably a better deal. A profits interest gives the holder a share of the value the company creates after the grant date, but no claim on the value that existed before it. The mechanism is a liquidation threshold: the company’s value on the grant date is recorded, and the holder participates only in proceeds above that line.

A worked example

An LLC worth $2 million grants a key employee a 5% profits interest with a $2 million threshold. Years later the company sells for $10 million. The first $2 million belongs to the pre-existing members; the employee’s 5% applies to the $8 million of growth, paying out $400,000. Had the company sold for exactly $2 million, the employee would receive nothing – they held a stake in the upside only. Illustrative numbers, real mechanics.

Under long-standing IRS guidance, a properly structured profits interest can be received tax-free at grant — no income on day one, and the potential for long-term capital gain treatment on the eventual payout. But the safe harbor leans on one fact: the liquidation threshold must be set at or above the company’s fair market value on the grant date. Set the threshold below true value and the interest stops being a pure profits interest; the recipient has effectively received existing value, and the tax-free grant treatment is at risk.

What LLCs cannot grant

Incentive stock options (ISOs) are available only for corporate stock, so an LLC taxed as a partnership cannot grant them – and the ISO reporting regime (Form 3921) never applies. LLCs that want option-like awards use unit options or unit appreciation rights, which work mechanically like their corporate cousins but are taxed under partnership rules. Phantom equity – a cash bonus contractually pegged to company value – is the other common route, popular because it creates no actual members and no K-1s, at the cost of ordinary income treatment for the recipient.

The hidden cost: every member gets a K-1

Granting real equity in an LLC makes the recipient a partner for tax purposes. That means a Schedule K-1 every year, possible state filings in every state where the company operates, and – because partners generally cannot also be W-2 employees of the same partnership – changes to how the person is paid. Companies planning broad employee ownership often weigh this administrative weight against the tax elegance of profits interests, and some choose phantom equity or convert to a corporation instead.

LLC vs. corporation: a practical comparison

|

Dimension

|

LLC

|

C corporation

|

|---|---|---|

|

Owners

|

Members holding units; flexible classes defined by the operating agreement

|

Shareholders holding stock; classes defined in the charter

|

|

Default federal tax

|

Pass-through (disregarded or partnership); no entity-level income tax

|

Entity pays corporate tax; dividends taxed again to shareholders

|

|

Profit splits

|

Fully contractual - can differ from ownership percentages

|

Generally proportional to shares within each class

|

|

Equity compensation

|

Profits interests, unit options, phantom equity; no ISOs

|

ISOs, NSOs, RSUs - the standard startup toolkit

|

|

Venture capital

|

Most institutional funds will not invest in pass-throughs; conversion usually required

|

The expected structure for VC-backed companies

|

|

Formalities

|

Light - no required board or annual meetings in most states

|

Board, bylaws, minutes, annual meetings

|

|

Ongoing paperwork

|

K-1s for every member each year

|

W-2s and 1099-DIVs; no K-1s

|

The pattern in practice: businesses built to distribute profit to a small group of owners – services firms, real estate, family companies – tend to thrive as LLCs. Businesses built to reinvest everything, grant broad employee equity, and raise institutional capital tend to be corporations, or LLCs that convert when the fundraise arrives.

Advantages and trade-offs

Why owners choose the LLC

- One layer of tax by default. Profit is taxed once, at the member level, rather than at the entity and again on dividends.

- Contractual flexibility. Profit splits, management rights, and exit terms are whatever the members agree to in writing.

- Losses can flow through. Subject to basis and other limits, early-year losses may offset members' other income - something a C corporation's losses can never do.

- Light formalities. No mandatory board meetings or minutes in most states, though good records remain wise for the liability shield.

- Profits interests. A uniquely tax-efficient way to give key people a stake in future growth.

Where the structure costs you

- Self-employment tax on active members. Pass-through profit for working owners generally bears employment taxes that corporate dividends do not.

- Tax on phantom income. Members owe tax on allocated profit even when no cash is distributed.

- K-1 complexity. Partnership returns are genuinely harder than corporate ones, and every new member adds filings.

- Fundraising friction. Institutional venture investors generally require a C corporation, forcing a conversion at exactly the moment the company is busiest.

- State-level costs. Annual franchise taxes and fees apply in several states regardless of profitability.

How to form an LLC, step by step

Formation is genuinely simple – which is part of why the structure is so popular. The steps below are the common path; details vary by state.

Choose the formation state. Most small businesses should form where they actually operate; forming elsewhere usually just adds a foreign registration and a second set of fees.

Name the company and appoint a registered agent. The name must be distinguishable in your state's records, and the registered agent is the official address for legal notices.

File the formation document. Called Articles of Organization or a Certificate of Formation depending on the state, filed with the Secretary of State for a fee.

Draft the operating agreement. Even single-member LLCs should have one - it is the document that proves the entity is real and governs everything the statute leaves open.

Get an EIN and open a business bank account. The employer identification number is free from the IRS, and the separate account is the first line of defense for the liability shield.

Decide the tax classification. Accept the default, or file the election for S or C corporation treatment if the analysis supports it - ideally with a CPA in the room.

Register where you operate and stay current. Foreign registrations, annual reports, franchise taxes, and any required licenses keep the company in good standing.

Parth Shah, Managing Director

(CPA-US · FCA · RV-S&FA · DISA)

Parth Shah leads Countsure’s CPA-led accounting, tax, and valuation practice, helping founders and owners choose the right entity structure and tax classification from day one.

Frequently asked questions

It protects your personal assets from the business’s debts and liabilities – a lawsuit against the company, a lease it cannot pay, a loan it defaults on. It does not protect you from your own negligence or fraud, from obligations you personally guaranteed, or from payroll taxes withheld from employees, which carry personal liability for the people responsible.

By default, no federal income tax at the entity level. A single-member LLC is reported on the owner’s return, and a multi-member LLC files an information return with profit flowing to members on K-1s. The LLC can elect S or C corporation treatment, which changes this – and several states charge LLCs franchise taxes or fees regardless of the federal picture.

Both give the holder a stake in future growth above a baseline. A stock option requires the holder to pay a strike price to buy shares; a profits interest requires no purchase – the holder simply participates above the liquidation threshold. Properly structured, a profits interest can be tax-free at grant, provided the threshold is set at or above the company’s fair market value on the grant date.

No. Incentive stock options exist only for corporate stock, so an LLC taxed as a partnership cannot grant them and never files Form 3921. The closest equivalents are profits interests and unit options, or phantom equity if the company wants to avoid making employees partners.

Institutional funds generally cannot or will not hold pass-through interests: K-1s create tax complications for their own investors, and the standard venture toolkit – preferred stock, ISOs, qualified small business stock treatment – is built on corporate stock. LLCs raising institutional capital usually convert, and the company’s value at conversion becomes the baseline for the new equity.

A sole proprietorship costs nothing to maintain but leaves your personal assets exposed to every business obligation. The moment the business signs contracts, takes on debt, hires anyone, or serves customers who could sue, the LLC’s liability shield usually justifies the modest formation and annual costs. The federal tax picture for a single-member LLC is identical to a sole proprietorship by default, so the decision is really about protection, not tax.

Get Started

Choosing a structure or weighing a tax election? Get it right the first time.

Countsure’s CPA-led team helps owners think through entity choice, tax classification elections, and the filings that follow – so the structure you pick today still works when the business grows.

- Entity choice mapped to how you actually operate

- S-corp and C-corp election analysis

- Profits-interest and equity-plan structuring

- Filings, EIN, and good-standing maintenance