⬤ Employee Guide

Employee Stock Options: A 409A Valuation Guide

Employee stock options help attract talent by giving employees ownership and aligning them with long-term company success.

Demystifying Employee Stock Options: A 409A Valuation Guide

This guide acts as a straightforward, friendly resource that founders can share directly with their teams to explain how stock options work. Understanding equity compensation empowers your employees to make informed decisions about their financial futures, while reinforcing the value of the benefits you provide.

By reading this guide, you will learn the mechanics of vesting, the difference between option types, and why a compliant 409A valuation is absolutely critical for your financial security. For a broader look at managing your company’s capitalization, we highly recommend mastering startup equity structures.

Want to ensure Your Option Plan is IRS-Compliant?

Contact CountSure today for a free 30-minute consultation!

What Are Employee Stock Options?

Employee stock options give an individual the right, but not the obligation, to buy a specific number of company shares at a locked-in “strike price” after a certain period. This equity compensation allows employees to share in the financial upside if the company grows and becomes more valuable over time.

This post serves as a foundational 409A valuation employee guide. It helps your team understand the true value of their equity and the mechanisms behind it. When learning about equity, it is also important to understand the difference between ISO and NSO stock options, as these two main types of equity carry very different tax implications upon exercise and sale.

How Do Stock Options Work? The Lifecycle of Equity

The lifecycle of an employee stock option involves three main phases. Understanding each step ensures you know exactly how and when your equity gains value.

01

The Grant and Strike Price

The process begins on the grant date, which is when the company formally awards you the stock options. At this time, your options are assigned a strike price. This is the predetermined, fixed price you will eventually pay to purchase the shares.

The strike price must be based on an independent, IRS-compliant valuation to ensure it reflects the true Fair Market Value (FMV) of the company's common stock at the time of the grant. This guarantees the options are issued legally and protects the option holder from adverse tax consequences.

02

Vesting Schedules and Cliffs

You do not receive full ownership of your options on day one. Instead, you earn them over time through a vesting schedule. The tech industry standard is a four-year vesting schedule paired with a one-year cliff.

For example, imagine an employee receives a grant of 10,000 shares. Under a standard schedule with a one-year cliff, zero shares vest during the first 12 months. On their one-year work anniversary, 25% of the grant (2,500 shares) vests immediately. After that cliff, the remaining 7,500 shares will vest in equal monthly increments over the next 36 months.

03

Exercising Your Options

Exercising your options means officially purchasing the vested shares at your locked-in strike price. This requires a financial commitment from the employee. If your strike price is $2 and you wish to exercise 1,000 vested options, you must pay the company $2,000. Once you exercise, you transition from being an option holder to an official shareholder of the company.

Example - 10,000 Share Grant

YEAR 1 CLIFF

MONTHLY VESTING – YEARS 2, 3 & 4

Shares — Months 1–11

0

+

Vest at 1-Year Cliff

0

+

Over 36 Months

0

+

Protecting Employees from 409A Penalties

Many employees do not realize the financial danger they face if founders mismanage valuations. If a company issues options below Fair Market Value, the employee pays the price.

The IRS enforces strict rules under Section 409A of the Internal Revenue Code. If an audit reveals that options were granted at a discount, the affected employees face severe IRS 409A tax penalties. These penalties include the immediate taxation of all vested options, plus a devastating 20% penalty tax on the stock options, along with potential state penalties and interest.

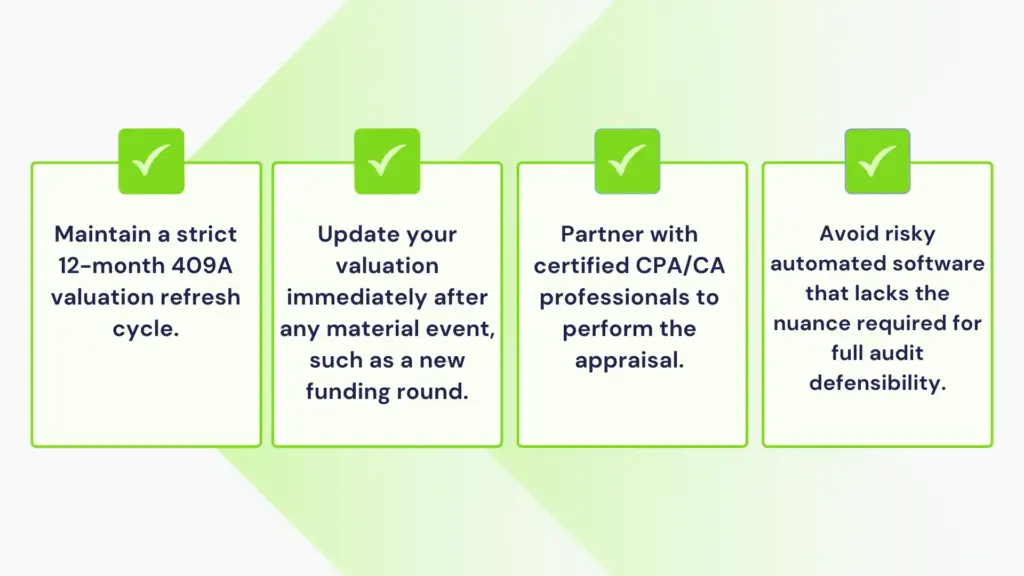

Founders Can Easily Protect Their Teams by Following a Strict Compliance Checklist:

Don't Put Your Employees' Financial Futures at Risk with Outdated Valuations.

Schedule your free 409A consultation with our certified CPAs.

Expert's Insights - Parth Shah, Managing Director

(CPA-US, FCA, RV-S&FA, DISA)

Founders often view 409A valuations as a mere compliance checkbox, but it is fundamentally an employee protection measure. Issuing employee stock options without a defensible, audit-ready 409A valuation exposes your top talent to severe IRS penalties. At CountSure, our CPA-led approach guarantees 100% auditor acceptance, ensuring your team’s equity remains a true benefit, not a hidden tax liability.

Frequently Asked Questions (FAQs)

An employee stock option is equity compensation that gives an employee the right to purchase a set number of company shares at a predetermined strike price after a specific vesting period.

A 409A valuation determines the Fair Market Value of the company’s common stock. This sets the legal strike price for your options to ensure they are not granted at a discount, which protects you from IRS penalties.

If a company violates 409A rules by issuing options below Fair Market Value, the employee faces severe IRS 409A tax penalties. This includes ordinary income tax on vested options, plus an additional 20% penalty tax.

Incentive Stock Options (ISOs) offer favorable tax treatment, potentially allowing the employee to pay only long-term capital gains tax if specific holding periods are met. Non-Qualified Stock Options (NSOs) are taxed as ordinary income upon exercise.

Most standard equity plans provide a 90-day Post-Termination Exercise window to purchase your vested options after leaving. However, some modern startups extend this window to provide greater flexibility.

A vesting cliff is a waiting period before any of your options become exercisable. A typical cliff lasts one year, after which the first major portion (usually 25%) of your option grant vests all at once.

Founders can protect their employees by securing timely, expert-led 409A valuations from certified professionals like CountSure. Maintaining a 12-month valuation refresh cycle guarantees IRS safe harbor protection.

Securing Your Safe Harbor Status

Communicating equity clearly to your employees builds trust and alignment. By educating your team on how stock options work, you reinforce the value of their compensation package and keep them motivated toward long-term goals.

Expert-led, fixed-fee 409A valuations are the safest way to issue employee stock options. By partnering with experienced CPAs, founders can confidently prepare for a new funding round or an annual 409A refresh, knowing their equity plan is fully compliant and their employees are protected.