⬤ IRS-Compliant Valuations

The 8 Factors of

Revenue Ruling 59-60

What Every Business Owner Must Know

Understand how the IRS values your closely held business and what it means for your estate, succession, or sale.

IRS · Rev. Rul. 59-60

Fair Market Value

Appraisal Report

Appraisal Report

IRS

CERT

CERT

FMV Appraisal

Audit-Ready

Zero Penalties

IRS Audit Record

1–2 Weeks

Turnaround

━━ The Foundation

Why Revenue Ruling 59-60 Matters for Your Business

Issued in 1959, Revenue Ruling 59-60 remains the gold standard utilized by the IRS and courts to determine the fair market value of private, closely held businesses. Whether you are navigating estate planning, gifting equity, preparing for an M&A transaction, or facing an IRS audit, understanding this ruling is essential.

For business owners, shareholders, and successors, adhering to this IRS-compliant valuation framework is the most effective way to ensure tax efficiency and prevent costly legal disputes.

Fair Market Value is the price at which property would change hands between a willing buyer and a willing seller, both having reasonable knowledge of relevant facts and neither under compulsion to act.

IRS Revenue Ruling 59-60

━━ Quick Overview ━━

The 8 Factors at a Glance

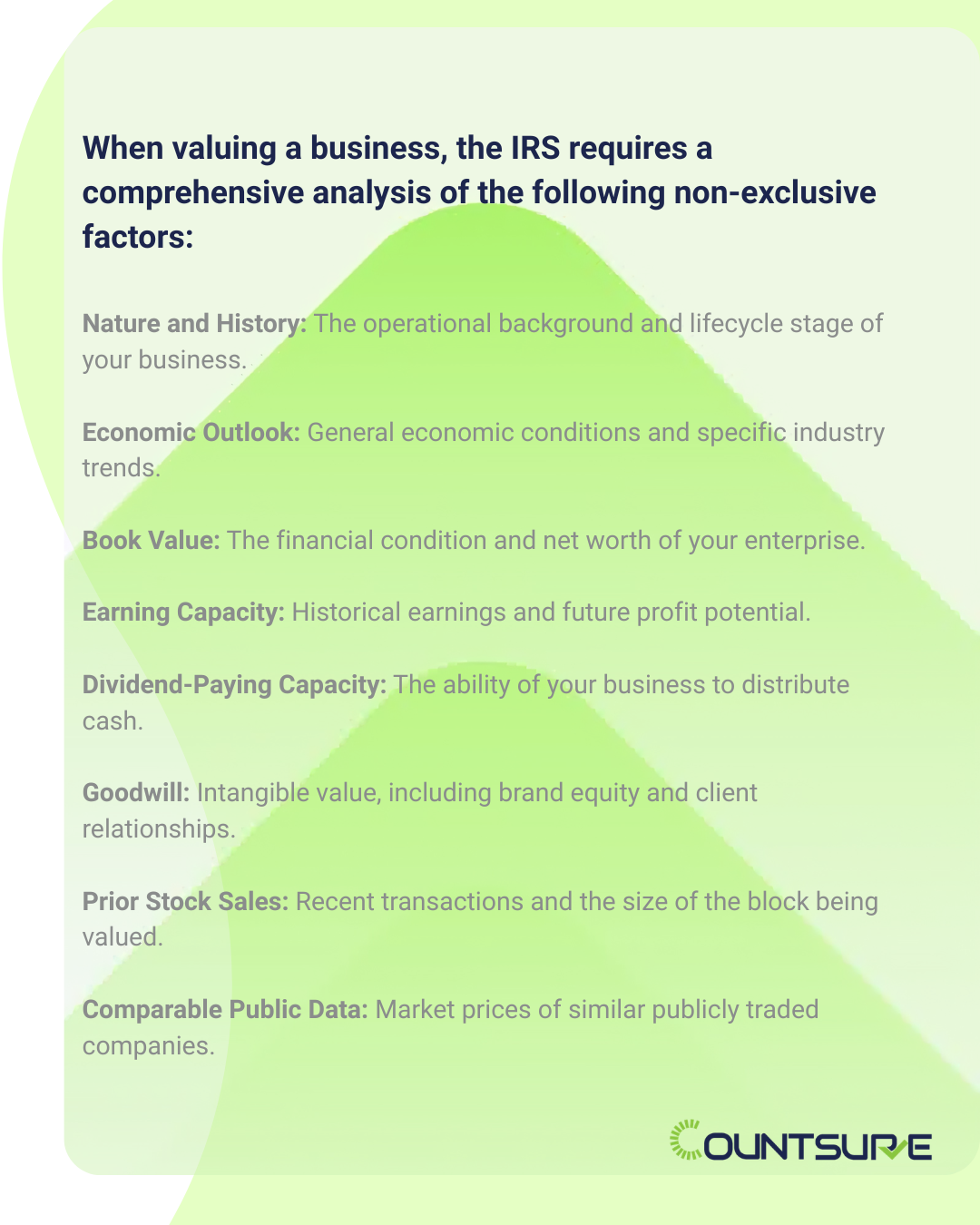

When valuing a business, the IRS requires a comprehensive analysis of the following non-exclusive factors.

Ready to Simplify Your Valuation Operations?

Let’s talk about how we can help your firm scale smarter.

━━ Deep Dive ━━

The 8 Valuation Factors Explained

Each factor plays a distinct role in determining the defensible, audit-ready value of your closely held business.

Nature & History of the Business

This factor examines your company's formation, ownership structure, and operational history. Establishing a stable, well-documented history reduces perceived risk a business that has successfully navigated past economic downturns will generally command a stronger valuation.

Economic Outlook & Industry Conditions

Valuations do not happen in a vacuum. This factor evaluates how macroeconomic trends and industry-specific conditions impact your business. Regulatory headwinds may pull value downward; operating in a high-growth sector can boost your baseline.

Book Value & Financial Condition

While book value provides a baseline, it rarely represents fair market value especially for service-based businesses. The IRS looks at your balance sheet to assess liquidity and financial health. Clean, audited financials are critical to maximizing this factor.

Earning Capacity

Often the most significant factor for operating companies, this looks at historical profit and future earning potential. For professional practices, normalizing owner compensation is critical stripping away discretionary expenses to reveal true profitability.

Dividend-Paying Capacity

The IRS focuses on your business's capacity to generate and distribute cash regardless of whether you actually pay dividends. Strong free cash flow signals a more attractive investment to a hypothetical buyer and commands a higher valuation.

Goodwill & Intangible Assets

Intangibles like brand reputation, patented technology, and loyal client lists significantly impact value. A common question: is goodwill tied to the enterprise itself or to the owner's personal reputation? A critical distinction in transition planning.

Prior Stock Sales & Block Size

Recent arm's-length transactions involving your company's stock provide concrete valuation evidence. The IRS also considers the size of the block being valued minority interests typically warrant a discount, while controlling interests may carry a premium.

Market Price of Comparable Public Stocks

When available, appraisers analyze market data of comparable public companies. Because your private company lacks the liquidity of public stock, a Discount for Lack of Marketability (DLOM) is often applied to bridge the gap between public multiples and private realities.

━━ Real-World Impact ━━

Why These Factors for Your Business Matter for Your Business

Each factor plays a distinct role in determining the defensible, audit-ready value of your closely held business.

Estate & Gift Tax

A defensible valuation ensures you do not overpay taxes on transferred wealth and protects you from IRS penalties.

Succession Planningess

Understanding your value helps structure buy-sell agreements and smooths the transition to the next generation.

M&A & Buyouts

Objective valuations based on these 8 factors prevent shareholder disputes and set realistic expectations for a sale.

IRS Audit Defense

An appraisal rooted firmly in Rev. Rul. 59-60 is your strongest shield against aggressive IRS challenges.

━━ Costly Errors ━━

Common Mistakes Business Owners Make

Avoid these pitfalls that can trigger audits, penalties, and shareholder disputes.

Relying on rigid rules of thumb or simplistic revenue multiples to determine your business value.

Failing to normalize financial statements to reflect true operational earnings and profitability.

Ignoring the necessity of minority interest discounts (DLOC) and marketability discounts (DLOM).

Attempting a DIY valuation instead of securing a defensible, AICPA-certified appraisal.

━━ Common Questions ━━

Frequently Asked Questions

Yes. Despite being issued in 1959, Revenue Ruling 59-60 remains the foundational authority relied upon by the IRS, courts, and valuation professionals to determine the fair market value of closely held businesses. Its eight-factor framework continues to shape every defensible appraisal.

It is recommended to obtain a formal valuation whenever equity is issued, gifted, or transferred or annually if you operate a stock option plan or have an active buy-sell agreement. Regular valuations keep your records defensible and your planning current.

You will typically need 3 to 5 years of historical financial statements, tax returns, current year-to-date financials, projected financials, organizational documents (such as operating agreements), and details regarding any previous equity transactions or ownership changes.

Costs vary based on the complexity and size of the business, but investing in a certified, IRS-compliant appraisal pays for itself by mitigating audit risks and optimizing tax strategies. Contact us for a precise quote during your free consultation.

Get Started

Protect Your Estate: Get an IRS-Compliant Valuation Today

Talk to a certified expert and get started in 24 hours. No obligation. 100% confidential.

- No obligation consultation

- Response within 12 hours

- 100% confidential

- IRS-compliant, audit-ready reports